According to a new report from Enterprise, length-of-rental (LOR) saw its first dip since the first stages of the COVID pandemic.

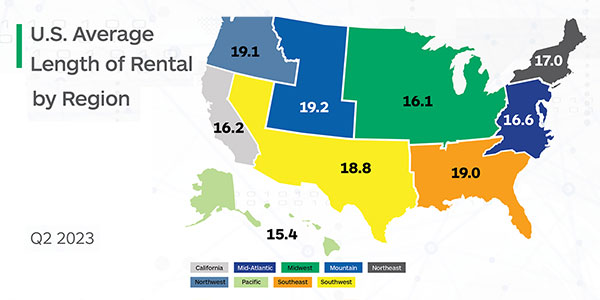

Q2 2023 U.S. LOR was 17.4 days, a 0.3-day drop from Q2 2022 (17.7). This is a 1.5-day decrease from Q1 2023 (18.7 days), which fits historical seasonal trending of a decrease from the 1st quarter of the year to the 2nd quarter.

While positive, Enterprise stated, these results continue to reflect the new normal, as LOR for Q2 2021 was 13.2 days.

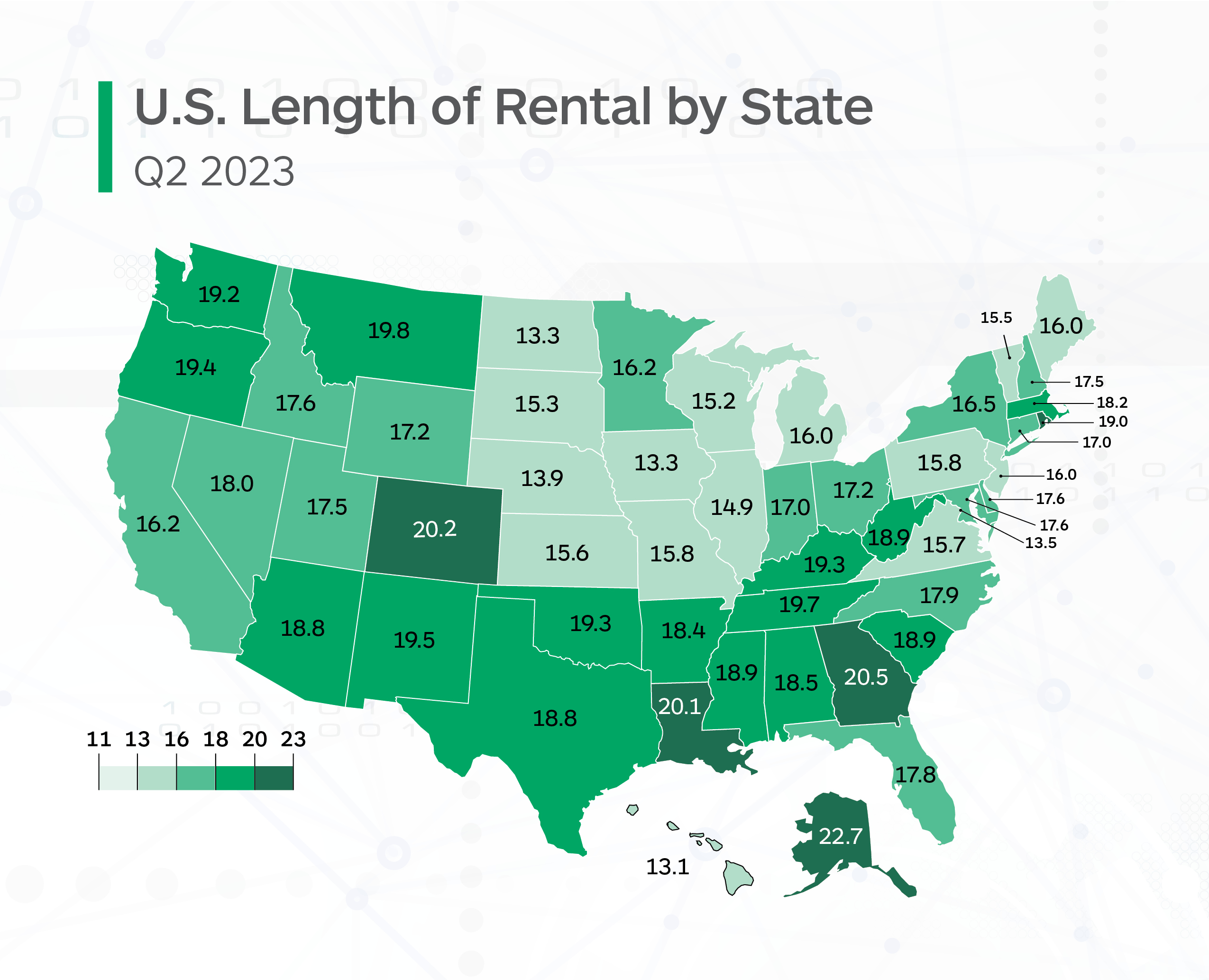

Alaska recorded the highest overall LOR in Q2 at 22.7 days, followed by Georgia (20.5), Colorado (20.2) and Louisiana (20.1). Hawaii had the lowest LOR with 13.1 days. North Dakota and Iowa were next-lowest at 13.3 days each, with DC (13.5) and Nebraska (13.9) completing the states under 14 days.

Interestingly, the gap between the highest (Alaska) and lowest (Hawaii) LORs was 9.6 days — compared to a gap of 9.0 days in Q2 2022. In the contiguous 48, the gap was 7.2 days between Georgia (20.5) and Iowa and North Dakota (both 13.1). In Q2 2022, this gap was 8.9 days between Louisiana and North Dakota.

Only three states saw a year-over-year increase of a day or more: Minnesota (+1.4), New Mexico (+1.2) and Montana (+1.0). Eighteen additional states saw increases while five other states were flat. Notably, 24 states, plus DC, saw decreases. Rhode Island (-2.0), DC (-1.9) and Louisiana (-1.8) had the largest decreases.

“We’re seeing a number of trends that could account for some — though not a lot — of decline in LOR, at least for now,” said John Yoswick, editor of the weekly CRASH Network newsletter. “Shops’ backlog of work tends to drop in the spring, and this year was no exception. The national average backlog was 4.7 weeks in Q2 2023, down from 5.8 weeks the prior quarter. Prior to the pandemic, the typical second quarter decline in backlog was about three days. This year, the drop was almost eight days, and the percentage of shops that could schedule a job in two weeks or less increased 14 percentage points to 27 percent. While that is the highest percentage of shops with a ‘normal’ backlog since October of 2021, it is still far from the pre-pandemic second quarter average of 72%. Nearly half of all shops (46%) were still scheduling work four or more weeks into the future. That is a significant decline from 60% in the first quarter of this year, but also far from the typical 7% with that length of backlog pre-pandemic.”

Added PartsTrader Chief Innovation Officer Greg Horn, “The overall Q2 2023 measure of median plus two standard deviations of delivery days for all part types was actually lower overall in Q2 2023 compared to Q2 2022; several state-level increases align with the LOR results. States that saw increases in overall LOR in Enterprise’s data, such as Arkansas, Florida, Georgia and Minnesota, also saw similar trends when comparing parts delivery days. Parts delays are still a significant factor in repair time and length of rental, and shops are making a great effort to schedule repairs for drivable vehicles to maximize shop throughput.”

It’s also important to consider the impact from the luxury segment, both ICE and EV.

“Luxury make repair frequency increased nearly half a point to 13.28% of all repairable estimates in Q2 2023 compared to Q2 2022 (12.79%),” said Ryan Mandell, director of claims performance for Mitchell International. “On average, luxury vehicle estimates are written for nearly two additional labor hours (1.83) compared to common make vehicles, as well as an additional 1.3 replacement parts.”

Mandell also shared an important consideration about calibrations, which impact overall repair time: “The frequency of ADAS calibrations increased from 11.28% in Q2 2022 to 16.11% in Q2 2023.”

Drivable

For rentals associated with drivable repairs, LOR in Q2 2023 was 15.5 days, a 0.3-day increase.

Alaska also had the highest drivable LOR in Q2 2023 at 18.8 days. Georgia (18.6), Tennessee (17.8) and Louisiana (17.7) were the next-highest.

The lowest drivable LOR for was found in North Dakota (10.5), Hawaii (11.3), Iowa (11.6) and DC (11.8).

The highest year-over-year drivable increases were found in Minnesota (+1.6), Alaska (+1.5) and New Mexico (+1.2). Three other states (WA, AR, UT) had increases of one day or more. A total of 39 states had drivable increases, with only three flat and eight states, plus DC, showing drivable decreases.

Non-Drivable

LOR for non-drivable claims was 25.6, a 0.8-day decrease from Q2 2022.

Montana had the highest LOR at 36.0 days, a 3.1-day increase. Next highest was Alaska (35.4), followed by Colorado (32.2). All told, eight states had non-drivable LOR greater than 30 days, with six more states at 28 days or higher.

Oregon (31.5) had the highest increase at 3.3 days. Positively, only 13 states had non-drivable LOR increases, while 37 states plus DC had decreases. Compare this to Q2 2022, when every single state and DC had an increase of at least 1.2 days.

The lowest non-drivable LOR belonged to New York at 21.1 days, followed by DC (21.2), Iowa (21.6) and Nebraska (21.9). Delaware had the highest decrease, down 3.4 days. Rhode Island (-3.2), DC (-2.5) and Indiana (-2.4) also saw significant decreases.

Yoswick also offered some insights from his latest survey regarding repair and supplement approval times: “From about 500 shops who responded to a CRASH Network survey in June, the average time those shops spend waiting for

a supplement approval hit another record high in 2023, approaching times that are nearly double what they were pre-pandemic. Shops say they are waiting 4.9 days (on average) for an insurer to complete an in-shop inspection to approve repairs. Prior to 2020, that time was just 2.9 days. Wait times for a remote desk review — or ‘virtual inspections’ — are averaging 4.3 days, almost two full days longer than the 2.4-day average reported in 2018.”

According to the CRASH Network results, shops cite approval times — along with some continued parts availability issues — as contributing to having more jobs at some stage in process, a factor that generally cuts into overall productivity. Among the shops who shared data in CRASH Network’s June survey, the average shop had work in process (WIP) that is equal to 66% of their typical monthly volume. That’s down from the fourth quarter of 2022 when shops’ WIP was averaging 78% of their monthly volume. But the average WIP is still higher than it was a year earlier when shops’ WIP averaged 59% of their typical monthly volume.

Total Loss

For rentals associated with total loss claims, LOR was 16.5 days, a 0.8-day decrease over Q2 2022.

While Alaska had the highest results at 25.3 days (+5.1 days), the next highest was Kentucky at 20.3 days, followed by Montana at 20.0 days.

DC had the lowest total loss LOR at 13.5 days, followed by Nebraska at 14.5 days.

Total loss LOR varied greatly; excluding Alaska, the highest increases were Wyoming at +2.2 days and Maine at +2.1 days. Twenty states (less Alaska) had an increase of 0.9 days on average. However, 29 states plus DC had an average decrease of 1.6 days, with 17 states plus DC down an average of 2.2 days.

Summary

As the numbers show, the trend of “predictable” seasonal LOR continues. The LOR decrease is positive, and many repairers are finding ways to anticipate and operate in the new normal. However, challenging market conditions remain, and overall LOR remains significantly higher than it was pre-pandemic.

Enterprise is committed to partnering with insurers, repairers and suppliers on all of the issues impacting repair times and LOR. Through foundational support provided by the Enterprise Holdings Foundation, Enterprise is spearheading the Collision Engineering Program, designed to attract and develop entry-level talent to fill essential roles within the collision repair industry. Enterprise is thrilled to expand its longtime partnership with Ford Motor Company, through its philanthropic arm, the Ford Fund, to expand the program and help address this ongoing industry challenge.

For more information, visit beacollisionengineer.com.